The Ultimate Guide to Digital Wallet App Development

Scope of Work

Cash, cards, and even traditional bank visits are rapidly fading into the background. Today, just a few taps on a smartphone can complete a transaction. Digital wallet apps have redefined how people send, receive, and manage money making speed, convenience, and security a part of everyday life.

According to Grand View Research, the global mobile wallet market was valued at USD 7.42 billion in 2022 and is expected to surge to USD 51.53 billion by 2030. This exponential growth highlights how both consumers and businesses are shifting toward a cashless economy powered by fintech innovation and mobile first experiences.

In this guide, you’ll discover everything essential to digital wallet app development from must have features, tech stack recommendations, and the step by step development process to cost insights and how to choose the right mobile app development company for building a secure, scalable wallet solution. Let’s dive in.

What Is a Digital Wallet App?

A digital wallet app is a secure mobile application that stores users’ payment information such as credit/debit cards, bank accounts, and even digital currencies all in one centralized place. It removes the need for physical cards or cash by enabling fast, cashless transactions across online platforms, in store purchases, and peer to peer transfers.

Essentially, a digital wallet functions as a virtual version of a physical wallet, streamlining how users make payments, send money, and manage their financial activity. Beyond convenience, it enhances transaction security and supports financial compliance standards.

How Digital Wallet Apps Work

Digital wallet apps rely on several key technologies behind the scenes:

-

Data Storage & Tokenization: When users add card or bank details, sensitive information is encrypted and replaced with a unique token, ensuring real card data is never shared during transactions.

-

User Authentication: Before completing a payment, the app verifies identity through PIN, fingerprint, or facial recognition, preventing unauthorized access.

-

Secure Payment Processing: The wallet communicates with banks, card networks, or payment gateways through encrypted channels to process transactions in real time.

-

Transaction Tracking: Users get instant notifications and can view detailed transaction history directly within the app.

Modern digital wallets also support NFC, QR code payments, and other contactless technologies allowing users to pay simply by tapping or scanning with their mobile device.

Why You Should Launch a Digital Wallet App Now

Building a digital wallet app isn’t just following a fintech trend it’s a strategic move that helps businesses unlock customer insights, boost revenue, and gain a long term competitive advantage.

Own and Leverage Your Transaction Data

When you control the payment experience, you gain access to valuable transaction data insights that traditional card networks typically keep for themselves. This data reveals customer spending habits, preferences, and behavioral patterns, allowing you to optimize products, pricing, and marketing strategies with precision.

Reduce Transaction Costs & Improve Customer Retention

A custom digital wallet can significantly cut transaction fees often by 40–60% at scale compared to traditional payment processors.

Even better, users who store their payment information tend to shop more frequently because you remove friction from checkout.

A real world example: Starbucks. Its mobile wallet accounts for more than 25% of all in store purchases and enables personalized offers that standard payment methods can’t support.

Stay Competitive in a Rapidly Changing Market

Customer expectations are shifting fast. They now look for seamless, integrated payment experiences. Businesses that lack digital wallet capabilities risk losing customers to competitors who offer smoother checkout, built in loyalty programs, and instant refunds.

It’s no surprise that more companies are investing in digital wallet development to future proof their customer experience.

Turn These Advantages Into Reality

With years of experience in fintech and mobile app development, HomeNest Software can help you build a secure, intuitive, and scalable digital wallet that enhances convenience, boosts engagement, and strengthens customer loyalty.

Let’s create a payment experience your customers will love.

Must Have and Nice to Have Features for a Digital Wallet App

A great digital wallet app is more than a payment tool it must deliver convenience, transparency, and uncompromising security. Below is a refined breakdown of essential and advanced features that shape a user centric, high performing wallet app.

Core Functional Features

User Registration & KYC Verification

A secure onboarding flow is the foundation of every digital wallet. Users can sign up via phone number, email, or social logins, followed by KYC verification. This ensures compliance with financial regulations and maintains transaction integrity.

Bank Account & Card Integration

Smooth integration with banks, debit/credit cards, and payment gateways allows users to top up or withdraw funds instantly. A frictionless linking process builds trust and encourages ongoing usage.

Balance Management & Transaction History

Users should be able to view real time balances, track detailed transaction history, and download statements. This transparency enhances user confidence and financial control.

NFC & QR Code Payments

For fast, contactless payments, digital wallets must support QR code scanning and NFC tap to pay. These features are now essential for in store checkout experiences worldwide.

Peer to Peer (P2P) Transfers

Instant money transfers between users enhanced with saved contacts, quick send shortcuts, and P2P request options boost engagement and app stickiness.

Push Notifications & Rewards

Real time alerts for payments, offers, and cashback rewards keep users informed and engaged. Loyalty programs and gamified incentives significantly increase retention.

Advanced & Security Features

Multi Factor Authentication (Biometrics, OTP)

Fingerprint, facial recognition, and OTP based verification ensure that only authorized users can access or approve transactions.

AI Powered Fraud Detection

Artificial intelligence analyzes user behavior and transaction patterns to detect anomalies and prevent fraudulent activity in real time.

Tokenization & Data Encryption

Tokenization masks sensitive card details, while encryption secures data during storage and transmission forming the core of a secure wallet infrastructure.

Blockchain Integration

Some advanced wallets integrate blockchain for immutable transaction logging, improving transparency, security, and cross border trust.

Multi Currency & Cryptocurrency Support

As digital payments globalize, supporting multiple fiat currencies or crypto assets opens your app to broader markets and tech savvy users.

Admin Panel Features

User Management Dashboard

The admin panel acts as the operational hub enabling administrators to manage users, approve KYC documents, and monitor app activity.

Transaction Monitoring & Reporting

A robust dashboard helps track transaction volumes, revenue flows, and performance insights. Automated reporting assists in compliance and trend analysis.

Dispute Resolution System

A structured complaint and refund management system boosts customer satisfaction and ensures adherence to financial regulations.

Marketing & Loyalty Tools

Admins can launch promotions, referrals, and cashback campaigns directly from the backend. Personalized marketing drives stronger engagement and brand loyalty.

By combining core features, advanced security, and powerful admin tools, businesses can create a high trust digital payment ecosystem that drives adoption and stays ahead in the fast moving fintech landscape.

Build a Secure, Feature Rich Wallet App with Experienced Developers

Partner with HomeNest Software to integrate the essential, security, and admin features needed to deliver seamless payments and exceptional user trust. Let’s build your wallet app the right way.

Step by Step Digital Wallet App Development Process

Developing a digital wallet app requires a structured and highly regulated approach. While timelines vary based on features and compliance needs, the process typically follows the stages below:

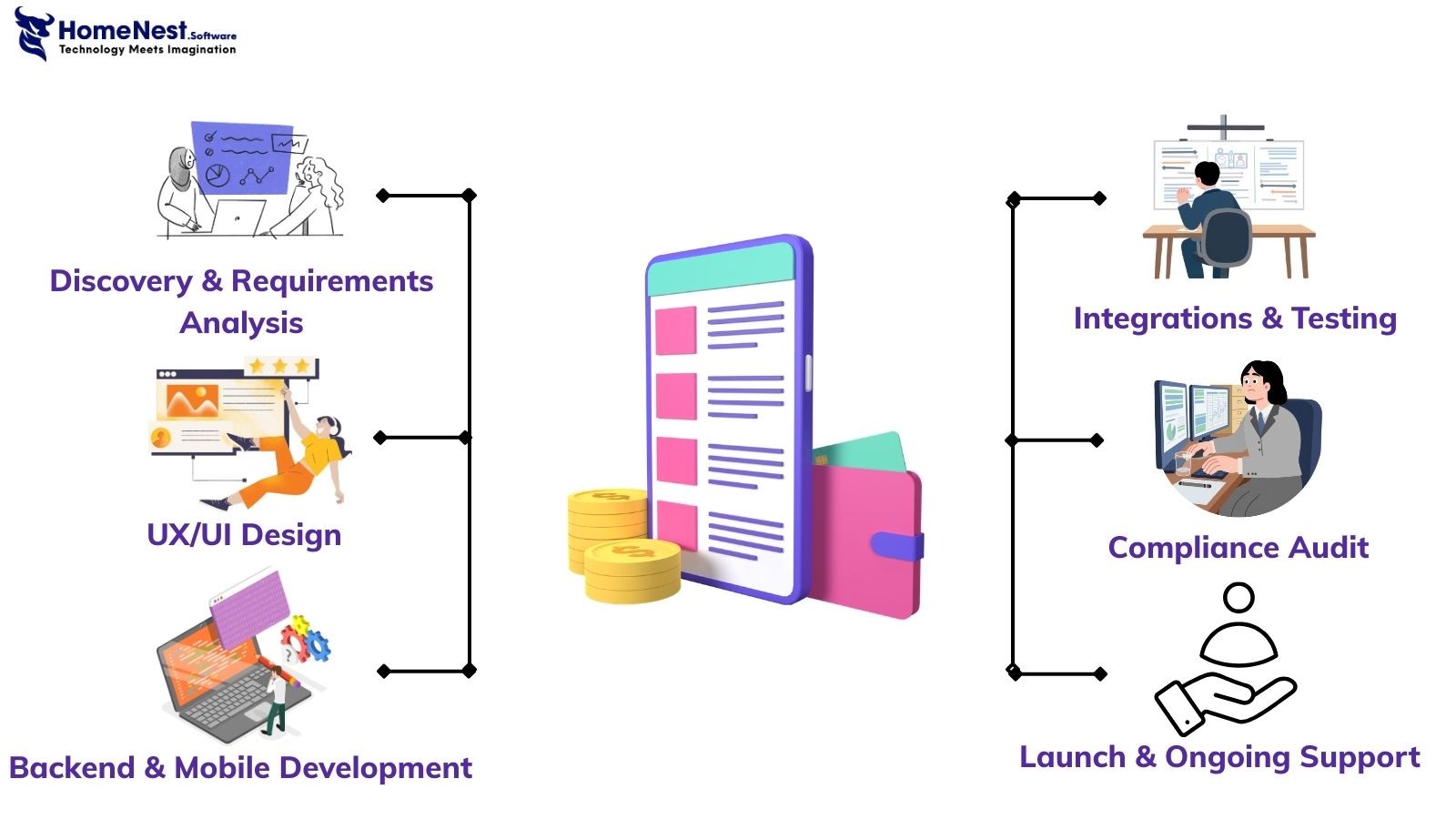

1. Discovery & Requirements Analysis

This phase focuses on understanding your market, users, and regulatory landscape.

You’ll analyze customer payment behaviors, identify gaps in competitor solutions, and assess compliance requirements across your target regions (e.g., U.S. vs EU vs APAC regulations).

Feature prioritization also happens here. Creating a feature matrix ranking features by user value and development effort helps define a clear MVP while planning future upgrades.

2. UX/UI Design

A seamless user journey is crucial. Mapping out the user flow from onboarding to first transaction ensures the experience is intuitive and fast. If users can’t complete payments in under 10 seconds, they’re likely to abandon the app.

Design steps include:

-

Wireframes to define structure and navigation

-

High fidelity UI design

-

Prototypes for real user testing

-

Accessibility standards (contrast, touch targets, screen reader support)

A user friendly interface directly impacts adoption and long term retention.

3. Backend & Mobile Development

The backend handles authentication, wallet balances, transaction processing, and integrations with banks or payment networks. Many teams use microservices for scalability and independent deployment.

Mobile development can be:

-

Native (Swift for iOS, Kotlin for Android)

-

Cross platform (React Native, Flutter)

Teams may hire iOS/Android developers or work with agencies like HomeNest Software for full stack development support.

4. Integrations & Testing

This stage connects essential third party services such as:

-

KYC/AML verification

-

Fraud detection APIs

-

Payment gateways

-

SMS/email notification systems

-

Analytics platforms

Testing includes:

-

Functional & integration testing

-

Security testing (penetration tests, vulnerability scans)

-

Load testing to handle peak transaction volumes

-

Device and OS compatibility testing

Given the financial nature of the app, security QA is significantly more rigorous than for a typical mobile app.

5. Compliance Audit

Compliance cannot be an afterthought.

Third party auditors typically validate:

-

PCI DSS (for card data handling)

-

AML/KYC controls

-

Data protection (GDPR, CCPA, etc.)

Audits often reveal areas requiring fixes, so aligning your architecture with compliance from the beginning reduces delays and costly rework.

6. Launch & Ongoing Support

Releasing a digital wallet involves meeting Apple and Google’s stricter requirements for financial apps including additional privacy, security, and encryption disclosures.

Post launch activities include:

-

Production monitoring (uptime, transaction success rates, crash logs)

-

Customer support for sensitive payment related issues

-

Regular updates for security patches and OS changes

-

Iterative feature improvements based on user feedback

Following this structured process ensures your digital wallet app is compliant, secure, scalable, and ready for real world financial operations.

Next, let’s break down the cost of developing a digital wallet app.

Cost Breakdown and Hidden Expenses

The cost of developing a digital wallet app varies widely depending on feature complexity, regional regulations, and whether you’re building from scratch or leveraging existing platforms. Below is a detailed cost breakdown to help you plan your budget effectively.

1. Development Hours and Rates

Building an MVP with essential payment features typically requires 2,000–3,000 development hours, covering UX/UI design, frontend and backend development, QA, and DevOps. A typical team includes:

-

Product Manager

-

UX/UI Designer

-

2–3 Mobile/Backend Developers

-

QA Engineer

-

DevOps Specialist

Hourly rates differ significantly by region:

| Region | Approx. Hourly Rate | Notes |

|---|---|---|

| North America (US/Canada) | $150–$200/hour | Highest cost, strongest fintech expertise |

| Western Europe | $100–$150/hour | Strong compliance knowledge (PSD2, GDPR) |

| Eastern Europe | $50–$100/hour | Cost effective, high engineering quality |

| Asia (India, Philippines, Indonesia) | $25–$50/hour | Affordable rates, large development talent pool |

| Vietnam | $20–$40/hour | Fast growing tech hub, strong mobile development ecosystem, excellent cost–performance ratio |

Estimated project cost:

-

North American team: $250,000–$400,000

-

Offshore team (Asia/Eastern Europe): $100,000–$200,000

-

Vietnam based team: $60,000–$150,000 depending on complexity

2. Third Party Service Costs

Digital wallets rely heavily on third party services, each adding operational costs:

-

Payment processors (Stripe, Adyen): ~2.9% + $0.30 per transaction

-

KYC/AML verification: $0.50–$3.00 per user check

-

SMS OTP / 2FA: $0.01–$0.05 per message

-

Cloud hosting (100,000 active users): $3,000–$8,000 per month

-

Security services (fraud detection, DDoS protection, monitoring): $1,000–$5,000 per month

These costs grow as your user base expands, particularly transaction and SMS fees.

3. Post Launch Maintenance

Many businesses underestimate long term costs. Expect to allocate:

-

15–20% of the initial development cost per year for maintenance

-

$5–$15 per user annually for customer support, especially for urgent payment related issues

-

Additional costs for OS updates, security patches, and new features

Want an Exact Cost for Your Wallet App?

Get a personalized, no obligation estimate from our experts to understand precisely what it costs to build a secure, scalable, feature rich wallet.

Tech Stack and Architecture Options

The technology choices you make directly affect development speed, performance, scalability, and long term operating costs.

Native vs Cross Platform Development

Native development (Swift for iOS, Kotlin for Android):

-

Best performance

-

Deep platform integration (Apple Pay, Google Pay)

-

Higher development cost (two separate codebases)

Cross platform (React Native, Flutter):

-

30–40% faster development

-

Near native performance for most features

-

Lower maintenance cost

| Approach | Development Time | Performance | Maintenance Complexity |

|---|---|---|---|

| Native | 6–9 months | Optimal | Higher (two codebases) |

| Cross Platform | 4–6 months | Near native | Lower (single codebase) |

Microservices and APIs

Monolithic systems may work for MVPs, but they struggle at scale. Microservices architecture modularizes your wallet into independent components authentication, payments, notifications which communicate via APIs.

Benefits include:

-

Independent deployment

-

Faster feature updates

-

Scaling only the services that need more resources (e.g., payment processing)

Cloud Infrastructure

Platforms like AWS, Azure, and Google Cloud offer powerful tools for fintech apps:

-

High availability

-

PCI DSS, GDPR, SOC2 compliance

-

Auto scaling and load balancing

-

Distributed hosting

Geographic hosting is critical: deploying servers closer to users (e.g., U.S., EU, Singapore, Vietnam) reduces latency and meets data residency rules.

Security and Compliance Checklist for Digital Wallet Apps

Fintech applications must comply with far stricter regulations than typical mobile apps. Failure to meet these standards can lead to heavy penalties, operational shutdowns, and even personal liability for leadership teams. Below are the core security and compliance requirements every wallet app must follow.

PCI DSS & PSD2 Compliance

PCI DSS (Payment Card Industry Data Security Standard)

Applies whenever your app stores, processes, or transmits cardholder data. It includes 12 requirements relating to:

-

Network and infrastructure security

-

Strong access controls

-

Data encryption standards

-

Continuous monitoring and auditing

Compliance ensures that card data is handled in a secure, standardized manner.

PSD2 (Payment Services Directive 2) For the European Market

If your wallet operates in the EU, PSD2 mandates:

-

Strong Customer Authentication (SCA) using multi factor verification

-

Secure, standardized APIs for Open Banking

-

Explicit user consent for sharing financial data with third parties

Wallets serving European users must integrate advanced authentication flows and secure API frameworks to meet PSD2 obligations.

KYC and AML Compliance

KYC (Know Your Customer)

Confirms user identity through government ID verification, address checks, and sometimes biometric validation.

AML (Anti Money Laundering)

Monitors transactions for suspicious patterns such as:

-

Large or unusual transfers

-

Rapid movement of funds between accounts

-

Transactions involving high risk regions

Third party providers like Jumio, Onfido, Persona, and others offer API based verification. However, even when outsourcing, your business remains legally responsible for compliance.

Data Encryption & Tokenization

Protecting sensitive data is mandatory for any financial application:

-

Encryption in transit: TLS 1.3

-

Encryption at rest: AES 256 or equivalent

-

Tokenization: Replaces real card numbers with random tokens that hold no exploitable value

Tokenization significantly reduces compliance burden because your system never stores raw card details. The real card information lives securely with the payment processor, while your app handles only tokens greatly minimizing exposure in case of a data breach.

If you’d like, I can also create a full compliance checklist table, a developer handoff version, or a risk assessment summary for your digital wallet app.

How to Monetize Your Digital Wallet App

Digital wallet apps offer multiple revenue opportunities, and the right monetization model depends on your target audience, transaction volume, and long term business strategy.

1. Transaction Fees

Charging 1–3% per transaction is the simplest revenue stream. Rates vary depending on payment type, processing partners, and total volume.

2. Interchange Fees

When users pay with stored cards, you can earn a share of the interchange fees paid by merchants, negotiated with issuing banks or card networks.

3. Subscription Plans

Premium tiers that include instant transfers, higher limits, advanced budgeting tools, or premium customer support can create predictable recurring revenue.

4. Merchant Partnerships

You can collect commissions from merchants who accept wallet payments or participate in exclusive deal programs, similar to loyalty driven ecosystems.

The strongest wallets combine multiple streams. PayPal, for example, earns from transaction fees, merchant services, held balance interest, and premium business plans. The key is balancing monetization with user experience excessive fees push users toward alternatives.

How to Choose the Right Digital Wallet Development Partner

Selecting the right mobile app development partner is critical, especially for fintech projects that require high security, regulatory expertise, and flawless execution. Thousands of agencies exist but only a fraction specialize in fintech.

Key Evaluation Criteria

Fintech expertise outweighs general development experience. Look for teams that:

-

Have built payment systems or wallet apps before

-

Understand financial regulations (PCI DSS, PSD2, KYC/AML)

-

Follow strict security practices and hold relevant certifications

Review their portfolio for similar projects and ask for case studies with proven results. Client testimonials especially from fintech companies reveal how they handle audits, compliance challenges, and technical hurdles.

Also, evaluate their methodology. Agile frameworks with frequent demos and iterative releases work best for digital wallets. Avoid teams that rely solely on waterfall processes.

Questions to Ask Your Vendor

Here are essential questions that reveal whether they truly understand wallet development:

-

How do you approach PCI DSS compliance and security testing?

-

What experience do you have in integrating specific payment networks or banking partners?

-

How do you handle support, maintenance, and updates after launch?

-

Who will work on the project senior engineers or junior developers?

-

What’s your typical timeline for a wallet app of similar complexity?

-

How do you manage scope changes or new feature requests?

The clarity and depth of their answers will show their professionalism and whether they’re equipped to build a secure, scalable fintech product.

Unlock Your Digital Wallet Vision with HomeNest Software

With experience serving 1,200+ clients, including complex fintech projects, HomeNest Software brings the technical expertise and regulatory insight needed for secure, scalable, and compliant digital wallet development.

Our approach goes beyond coding. We help you refine your feature set, validate your assumptions, and build a product that actually drives user adoption and revenue. Through agile development cycles, you’ll see working software quickly, allowing real world testing and rapid iteration no months long waits for the first version.

Ready to bring your digital wallet idea to life?

Contact HomeNest Software to explore custom finance software solutions that transform your concept into a secure, user friendly, and market ready wallet app.

Contact HomeNest Software today for a free consultation and inquire about our all inclusive App Design package offers!

HomeNest Software – Empowering Long Term Growth for Modern Businesses.

![]()

Contact Information:

- Address: The Sun Avenue, 28 Mai Chi Tho Street, Binh Trung Ward, Ho Chi Minh City

- Hotline: +84 898 994 298 ( WhatsApp )

- Website: homenest.software

HomeNest Services: Website Design – App Design – Software Development – Digital Marketing.

FAQ

1. How long does it take to develop a digital wallet app?

A standard digital wallet MVP typically takes 4–6 months to build. More advanced versions with features like crypto support, AI fraud detection, or multi currency wallets may take 8–12 months, depending on complexity and compliance requirements.

2. How much does it cost to build a digital wallet app?

Costs range from $60,000–$150,000 when developed by teams in Asia or Vietnam, and $250,000–$400,000 for teams in North America. The final cost depends on features, integrations, security requirements, and platform choices (native vs cross platform).

3. What security features should a digital wallet include?

A secure wallet app should use AES 256 encryption, TLS 1.3, tokenization, biometric login, multi factor authentication, and real time fraud detection. Additional compliance, like PCI DSS, KYC, AML, PSD2, may apply depending on the region.

4. Do I need PCI DSS certification for my wallet app?

You need PCI DSS compliance if your app stores, processes, or transmits card data. If you use a PCI compliant processor and only store tokens (not raw card numbers), your compliance burden is significantly reduced.

5. Can a digital wallet support multiple currencies or cryptocurrencies?

Yes. Modern digital wallets can support multi currency balances, cross border payments, and even crypto assets. However, this requires additional regulatory checks and a more complex backend architecture.

6. Should I build the app using native or cross platform technology?

-

Native (Swift/Kotlin): Better performance, deeper hardware integration

-

Cross platform (Flutter/React Native): Faster development, lower maintenance cost

Most businesses choose cross platform unless they need advanced, platform specific features.

7. What is the biggest challenge in digital wallet development?

The toughest challenges are security, fraud prevention, and regulatory compliance. Meeting PCI DSS, KYC/AML, data privacy laws, and passing third party audits often requires specialized fintech expertise.

8. How do digital wallet apps make money?

Wallet apps typically monetize through transaction fees, interchange revenue, subscriptions, merchant partnerships, cashback sponsorships, and value added financial services.

9. Can I integrate my wallet with banks or financial institutions?

Yes. Banks provide APIs for balance checks, transfers, and account linking. Depending on your region, you may need to comply with Open Banking, PSD2, or other financial API standards.

10. Why should I hire a fintech experienced development team?

Wallet apps require deep knowledge of security, payment networks, regulatory rules, and fraud prevention. A general mobile app team may struggle with compliance, leading to delays or costly rebuilds. A fintech focused partner ensures faster, safer execution.

Latest Articles

View All

Criteria For Choosing The Right App Design Agency

UI/UX design is the logical foundation of a system, not merely a visual element. Choosing the wrong partner will directly lead to technical debt, budget overruns, and disruptions in the development process. This article provides a 6-step evaluation framework and a list of operational risks, helping businesses eliminate subjective design advice and accurately assess agency capabilities based on developer handoff standards and practical business performance.

How Does AI in Banking Industry Impact the Future?

Artificial intelligence (AI) has transitioned from a supplementary tool to a core infrastructure of financial data management, optimizing profitability through real-time fraud detection, natural language processing (NLP), and high-speed credit scoring models. “Deploying AI in the financial sector requires more than just algorithmic accuracy, it demands a highly secure cloud architecture and rigorous data governance,” commented Nguyen Tien, co-founder of HomeNest Software. Why read this guide? We skip the theoretical jargon to focus entirely on technical implementation. Whether you’re evaluating a vendor or planning a system overhaul, this article will detail: Operational Efficiency: Automating unstructured data workflows at scale. Risk Architecture: Implementing real-time threat detection and AML compliance. Data ownership: The essential need for 100% ownership of the source code to ensure full algorithm auditability.

How to Make a Banking App like Bank of America?

Developing a mobile banking application like Bank of America extends far beyond basic UI design; it requires engineering a fault-tolerant backend capable of real-time ledger synchronization, biometric authentication, and high-volume data processing under strict regulatory frameworks. Drawing from HomeNest Software’s deep experience in architecting enterprise-grade fintech solutions, this guide strips away theoretical jargon to focus entirely on operational and technical execution. What you will find in this guide: We break down the precise development roadmap, from mapping out microservices and ensuring PCI-DSS compliance to estimating MVP development costs and securing absolute data sovereignty through 100% source code ownership. If you are preparing to build, scale, or audit a financial platform, this blueprint provides the exact framework you need.

Banking App Development Cost

Building a banking application is rarely a simple process; it’s a complex technical challenge requiring a balance between complying with stringent financial regulations, handling large transaction volumes, and a scalable cloud architecture. Miscalculating these technical requirements from the outset often leads to significant technical debt and budget overruns. Based on HomeNest Software’s practical experience in designing enterprise-grade fintech solutions, this guide bypasses generic estimates to provide a realistic analysis of banking application development costs. What you’ll find in this guide: We analyze the true cost factors, from technology selection and API integration to the hidden costs of regulatory compliance and security infrastructure. Whether you’re launching a minimum viable product or expanding an existing financial platform, this analysis provides the precise operational data you need to plan your budget effectively.

How to Build a Mobile Banking App Like Chime?

Building a mobile banking app like Chime is not just about features, it is about delivering a secure, scalable, and user-centric financial experience. From planning the right architecture to optimizing mobile banking app development cost, every decision directly impacts your product’s success. Leveraging Fintech app development services, starting with MVP app development, and scaling through on-demand app development solutions allows businesses to reduce risk and accelerate time to market. To stay competitive, combining Android app development services and iOS app development solutions ensures wider reach, while continuous updates through maintenance software development services keep your app secure and future-ready.

How to Build a Banking App Like Barclays: A Complete Entrepreneur’s Guide

Building a banking app like Barclays requires more than just development. It demands a strong product vision, secure architecture, and a clear monetization strategy. From optimizing cost and selecting the right tech stack to ensuring compliance and scalability, every decision impacts long-term success. Partnering with an experienced team like HomeNest Software helps accelerate development, reduce risks, and deliver a high-quality fintech product that can compete in today’s fast-evolving digital banking landscape.